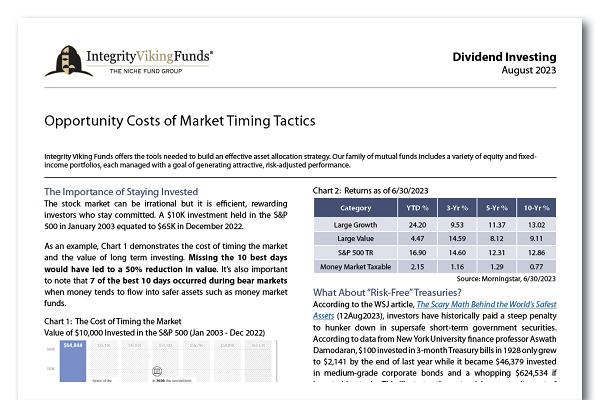

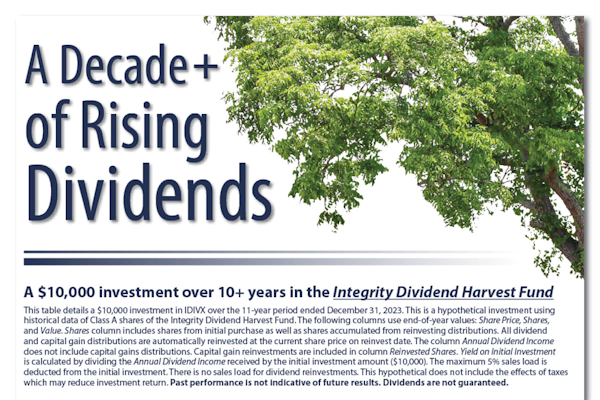

* There is no assurance or guarantee companies that issue dividends will declare or continue to pay or increase dividends. Past performance is not indicative of future returns.

The mutual funds of Integrity Viking Funds are distributed by Integrity Funds Distributor, LLC, Member  FINRA, and are available through licensed third-party Broker/Dealers. Integrity Funds Distributor, LLC is located at 1 Main Street North, Minot, ND 58703 (701) 852-5292.

FINRA, and are available through licensed third-party Broker/Dealers. Integrity Funds Distributor, LLC is located at 1 Main Street North, Minot, ND 58703 (701) 852-5292.

© 2024 Integrity Viking Funds